From Distribution to Ownership

Before we get started…if you want to learn more about bitcoin – connect with the Onramp MENA team.

And now, for the weekly roundup…

Morgan Stanley's Bitcoin ETF filing is the clearest signal yet that institutional demand has moved from curiosity to conviction.

Morgan Stanley's spot bitcoin ETF took a decisive step forward last week. On Tuesday March 24th, NYSE Arca posted an official listing notice for the Morgan Stanley Bitcoin Trust, ticker MSBT, and the bank filed Form 8-A to register its shares on the exchange. The amended S-1, filed March 18, had already locked in the operational details: Coinbase as prime broker and custodian, BNY Mellon handling cash and administration, a $1 million seed investment, and a six-month fee waiver on the first $5 billion. Now the product has a listing venue and a registration filing. What remains is final SEC approval.

Morgan Stanley Is Not an ETF Company

Every spot bitcoin ETF currently trading in the United States was created by an asset management firm. BlackRock, Fidelity, Invesco, VanEck, Bitwise. These are companies that build investment products for a living. Morgan Stanley is the largest wealth management provider in the world, with $9.3 trillion in total client assets across Wealth and Investment Management as of December 2025. Its wealth management arm is served by over 16,000 financial advisors who sit across the table from high-net-worth individuals, family offices, pension fund managers, and corporate treasurers every day.

Morgan Stanley does not launch many ETFs. It does not need to. The fact that it is building a proprietary bitcoin ETF is an extraordinary signal of internal client demand. Since August 2024, its financial advisors have been permitted to recommend existing third-party bitcoin ETFs, products where the management fee flows to BlackRock or Fidelity.

MSBT redirects that fee capture internally and gives Morgan Stanley full control over how bitcoin exposure is positioned, priced, and distributed across its advisory platform. The bank also plans to offer retail crypto spot trading in the first half of 2026. Amy Oldenburg, Morgan Stanley's head of digital assets strategy, highlighted at the Digital Asset Summit on March 24 that this is the result of years of infrastructure modernization. This is a coordinated institutional buildout.

The IBIT Benchmark

To understand what Morgan Stanley is aiming at, start with what BlackRock's IBIT has accomplished. IBIT launched in January 2024 and by many measures became the most successful financial product launch in history.

As of mid-March 2026, IBIT holds approximately $55 billion in AUM and $63.2 billion in total cumulative net inflows, roughly 45% of all AUM across every U.S. spot bitcoin ETF. During a six-day inflow streak in early March, IBIT captured 78% of total flows. On March 23, it accounted for 95.8% of the entire day's net positive activity. When institutional capital moves into bitcoin, it moves almost exclusively through BlackRock.

IBIT's dominance was built on a first-mover advantage that captured enormous latent demand. For years, a massive pool of institutional and advisory capital wanted bitcoin exposure but couldn't access it directly due to compliance constraints and custodial limitations. These allocators needed a familiar, regulated wrapper from a name they trusted. IBIT provided that. Much of the initial wave was pent-up and structural, released by the product's existence rather than generated through active solicitation.

The resilience during the recent drawdown is worth highlighting. Bitcoin has fallen over 40% from its October 2025 all-time high near $126,000, and spot ETFs endured their worst two-month outflow streak from November 2025 through January 2026, totaling approximately $6.2 billion in net redemptions.

But March reversed the trend sharply: approximately $2.5 billion in gross inflows, reducing YTD net outflows to just $210 million. Eric Balchunas of Bloomberg noted that when gold experienced a comparable 40% drawdown a decade ago, it lost a third of its investor base. Bitcoin ETFs have held.

What Morgan Stanley Brings

MSBT enters a market where IBIT has near-monopolistic flow dominance. Morgan Stanley cannot win by capturing the same latent demand IBIT already absorbed. It has to generate net new demand through active solicitation to its own client base and the broader wealth management industry.

The numbers illustrate the scale of that opportunity. Morgan Stanley recommends a 0 to 4% bitcoin allocation for eligible clients. Consider what even modest adoption looks like against their asset base:

A 0.5% average allocation across Morgan Stanley's wealth management client assets would represent more than $30 billion in new bitcoin demand, equivalent to roughly 430,000 BTC at current prices and larger than the AUM of any spot Bitcoin ETF other than IBIT.

A 1% allocation would represent more than $60 billion, rivaling IBIT's total cumulative inflows to date and equivalent to roughly 850,000 BTC.

A 2% allocation would represent over $120 billion, approaching the total AUM of the entire spot bitcoin ETF market today.

Of course, real flows will depend on advisor adoption rates, client risk appetite, regulatory approval timing, and competitive dynamics. But the directional point is unmistakable: Morgan Stanley's distribution network is large enough to reshape the bitcoin ETF landscape even at modest allocation levels.

The six-month fee waiver on the first $5 billion signals the bank is prepared to compete aggressively on price to build initial scale. And 16,000 financial advisors having relationship-driven conversations with clients who already trust the brand is a fundamentally different acquisition model than passive ETF inflows.

Bitcoin's Wartime Resilience

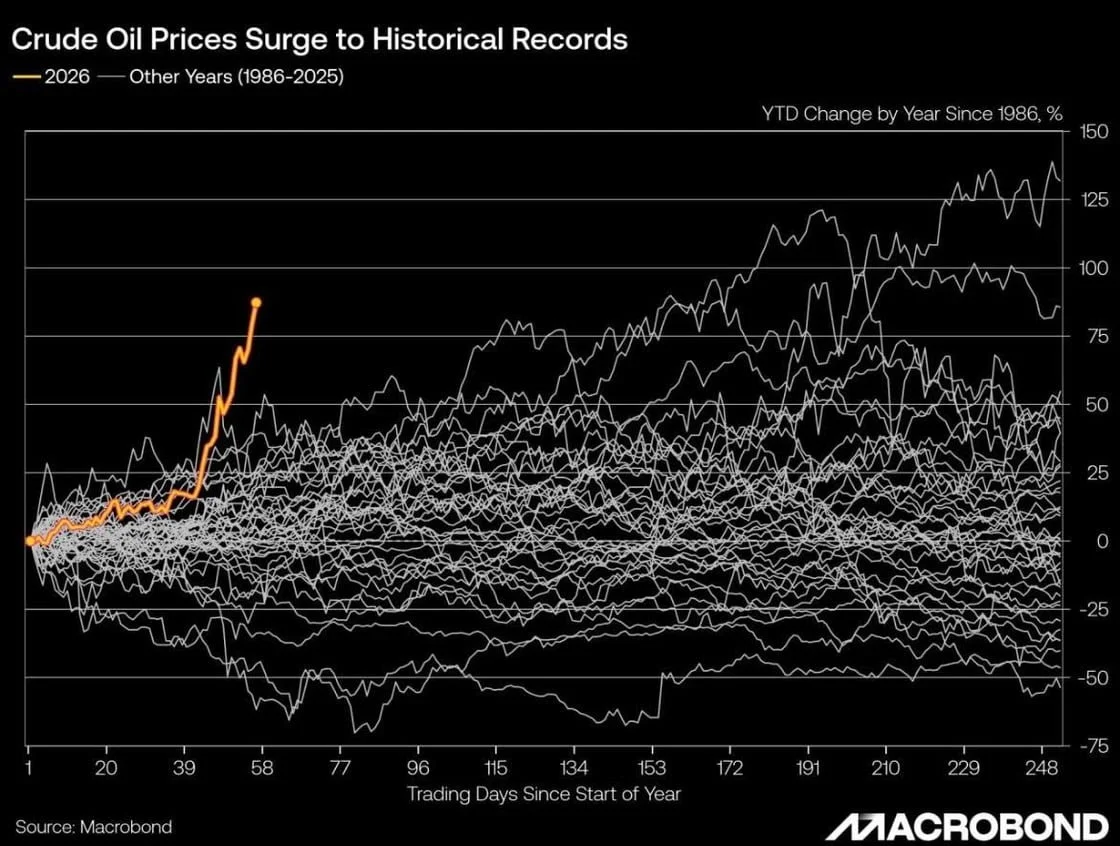

This filing arrives against a backdrop that would have been catastrophic for bitcoin in any prior cycle. The U.S. and Israel launched strikes against Iran beginning February 28. Brent crude remains elevated. The Strait of Hormuz remains closed to most international shipping.

The Fed, which had been cutting rates through the back half of 2025, was forced to pause its easing cycle at 3.50 to 3.75% as the energy shock reignited inflation concerns. A central bank that wanted to cut found itself unable to, pinned by a geopolitical conflict rewriting the inflation outlook in real time.

Yet bitcoin has held around the $65,000-70,000 range. It is on track to post its first positive monthly candle against gold in eight months, a notable reversal after gold's roughly 21% decline from its late January all-time high near $5,600.

The macro environment is stress-testing every asset class and violently reintroducing the realities of counterparty risk. What is emerging is a clearer picture of which assets hold up under that kind of pressure.

And while headlines focus on the drawdown from last year's highs, the institutional infrastructure being built underneath the surface tells a different story. ETF flows have nearly erased all 2026 outflows in a single month. And now the largest wealth manager on the planet is filing to put its own name on a bitcoin product and mobilizing 16,000 advisors to distribute it.

Markets will do what markets do. But the institutions building the rails are not waiting for permission from the price.

Chart Of The Week

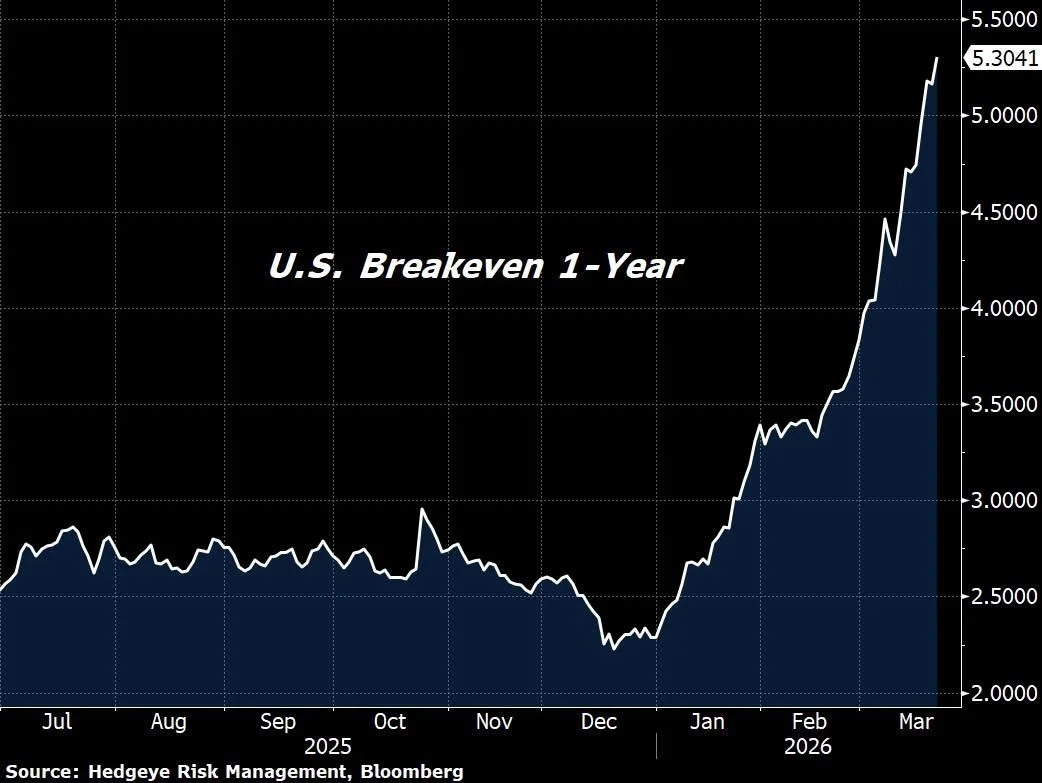

"The bond market sees inflation rising above 5.3% YoY over the next twelve months."

— Hedgeye on X

"Money is not merely a medium of exchange; it is also a signaling system that governs how societies allocate time, risk, and imagination."

Podcast Of The Week

Bitcoin For Professionals: The Money Truths Gen Z Refuses to Ignore

Gen Z is asking hard questions about money, the system, and the future of work.

Subscribe to Onramp MENA’s YouTube channel to catch new episodes of the Bitcoin For Professionals podcast!

Onramp MENA is an advisory and educational platform dedicated exclusively to Bitcoin.

If Onramp MENA’s offerings align with your needs, or those of someone you know, feel free to schedule a consultation with us here.