The Real Safe Haven

Operation Epic Fury is eight weeks old. Oil is up forty percent, gold is down, bonds are down, stocks are down, and bitcoin is the only major asset outside of the one directly tied to the conflict that has produced a positive return.

Below we unpack why this pattern has now repeated across seven consecutive macro shocks, why the variables that can impair a bitcoin position are shrinking while the variables impairing every other asset are multiplying, and what it means that a four-star admiral just described bitcoin as "a reality" in front of the Senate Armed Services Committee.

And now, for the weekly roundup…

Operation Epic Fury began on February 28th. What has happened in the eight weeks since is the exact stress scenario that asset allocation frameworks are built around, and most of those frameworks have failed it in real time.

Oil is up roughly forty percent, for the obvious reason that the conflict has direct implications for oil. Most stocks are flat to down a few percent. Gold, which spent most of 2025 being heralded as the safe-haven trade of the decade, is actually lower since the bombs started falling. Bonds, which are supposed to be the portfolio's shock absorber when equities sell off, have added to the damage rather than offset it.

The only major asset that has produced a positive return outside of the one directly leveraged to the physical conflict is bitcoin, which is up meaningfully off its recent lows, outperforming most other asset classes.

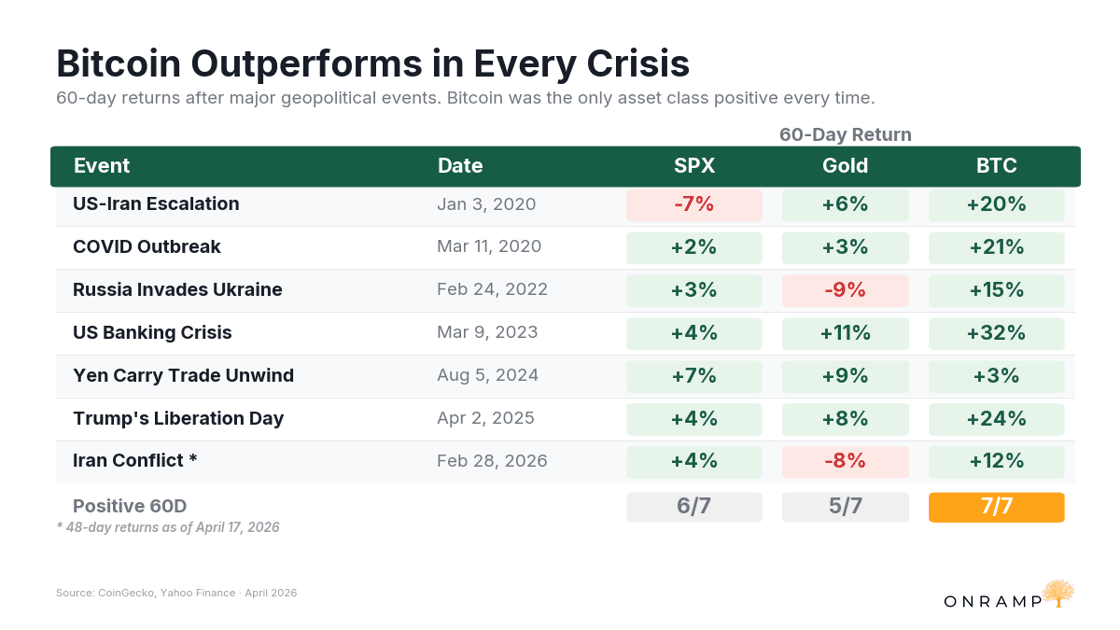

Going back through the seven largest macro and geopolitical shocks of the last six years, the COVID crash, the Russian invasion of Ukraine, the 2023 regional banking crisis, the yen carry trade unwind, Liberation Day tariffs, the June 2025 Iran flare-up, and now Epic Fury, bitcoin has produced positive sixty-day forward returns in every single instance. The S&P 500 managed six out of seven. Gold managed five. Bitcoin went seven for seven.

Seven data points is admittedly not conclusive, but it is enough to notice that the asset most continue to treat as speculative is the only one in the measurement window that has consistently shown resilience in the face of chaos.

Why This Keeps Happening

The usual explanation is that bitcoin is scarce, portable, and has no counterparty. True, but incomplete. The more relevant framing is that bitcoin is the only investable asset where the list of variables that can impair the position has been systematically compressed to something close to its theoretical minimum.

Every other asset you own is a claim on something, and every claim carries its own cloud of exogenous variables that you are implicitly underwriting whether you want to or not.

An equity is a bet on a management team, a regulatory regime, a capital structure, an industry cycle, a discount rate set by thirteen people in Washington, and the currency the earnings happen to be denominated in, all of which can move against you at any time and none of which you control.

A bond is a promise from a counterparty to return capital denominated in a unit of account that the counterparty prints.

Gold gets closer to ideal in its monetary properties but still carries custody risk, assay risk, confiscation risk, and the analog limitation of being a physical object in a digital economy.

Real estate is a concentrated bet on location, policy, and the banking system that finances it.

Every traditional asset, without exception, requires the holder to be right about dozens of variables that are becoming less and less predictable, as fiscal dominance, sanctions regimes, energy shocks, and monetary debasement compound on each other.

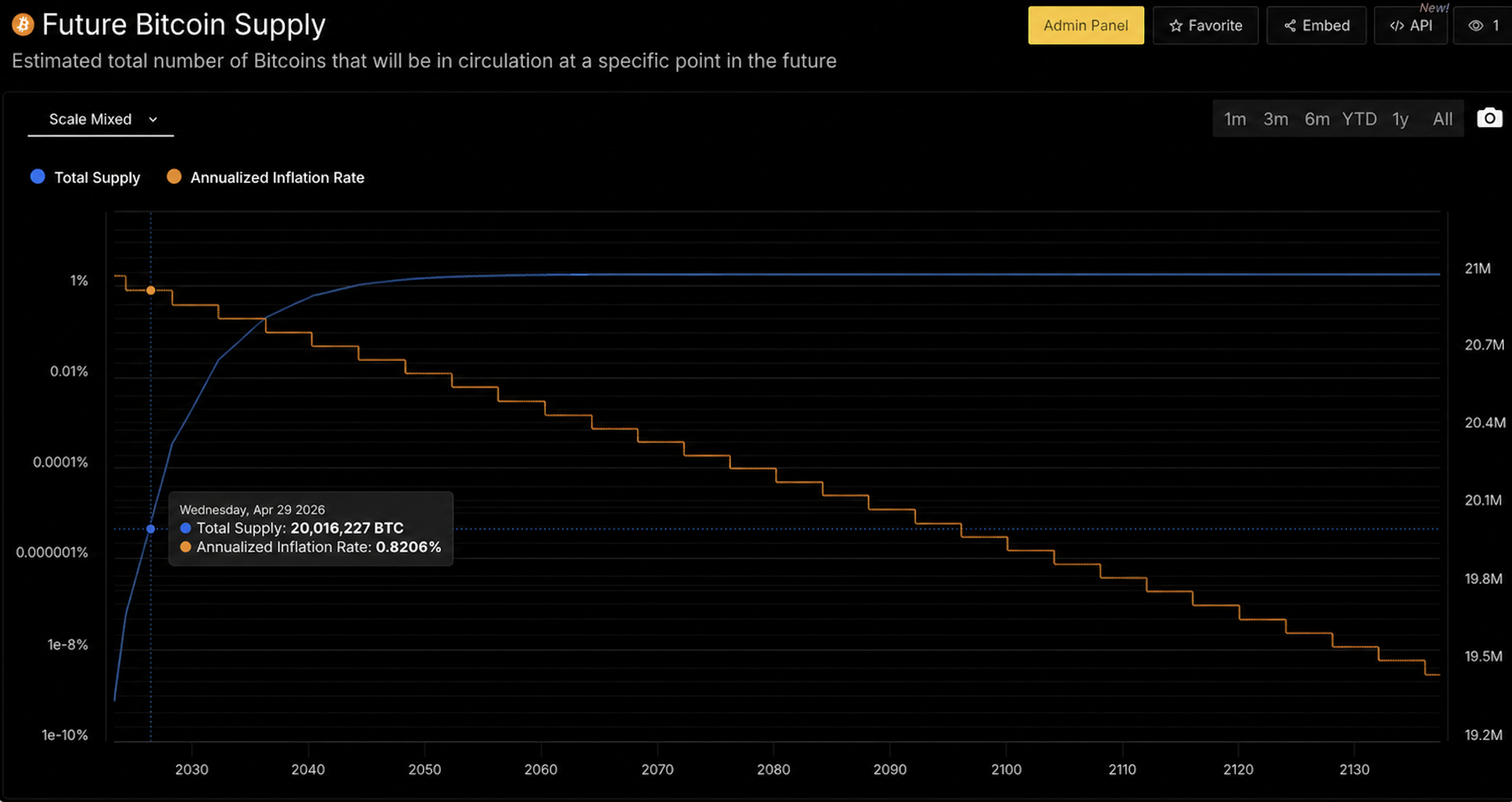

Bitcoin runs in the opposite direction. The supply is fixed at twenty-one million. The issuance schedule is public and auditable. The protocol is neutral and maintained by a globally distributed network that no single entity has shown the ability to capture. There is no management team to misallocate capital, no central bank to debase the unit, no jurisdiction to seize the underlying, and no counterparty whose solvency you have to monitor.

Onramp Bitcoin Terminal

What is left is a much shorter list of things you actually need to be right about: that the network continues to secure itself through proof-of-work, that adoption continues to trend in one direction over time, and that the properties that give the asset its value in the first place are preserved by the incentives of its participants. That list has not changed materially in seventeen years.

The practical result is that when the rest of the global portfolio is being pushed around by variables that were supposed to be exogenous to the investment thesis and turned out not to be, bitcoin sits there doing what it has always done. It is a unique asset that is structurally built to have fewer things that can go wrong in a world where more and more things are going wrong, and uncertaintly is at all-time highs.

The Sorting

If the macro picture is doing the work of validating bitcoin's monetary thesis, the internal dynamics of the broader digital asset market are doing the work of separating bitcoin from everything else that has been sharing its label.

Polymarket launched twenty-four seven perpetual futures. Prediction market volumes are setting records on contracts whose payoff structures are indistinguishable from sports betting. DeFi protocols are cycling through the usual rhythm of exploits, depegs, and forced liquidations, and the marketing has quietly shifted from "decentralized finance" to "onchain finance" because the first phrase was never accurate and the second is vague enough to survive scrutiny.

The large exchanges are promoting leveraged perps to retail. Tokens that spent the last cycle being sold as the next bitcoin are down seventy, eighty, ninety percent from their highs. And what's left of the "crypto" space (stablecoins, RWAs, etc.) is effectively being absorbed by traditional finance.

None of this is surprising, and none of it is new. What the industry has always called "crypto" was, and is, leveraged gambling dressed in the aesthetic of a monetary revolution. Two separate things have been sharing a label. One of them is a neutral settlement network with a fixed supply, a globally distributed validator set, and a seventeen-year track record of running without interruption. The other is a casino.

They have never been the same category, and the market is finally pricing the distinction. Flows are separating. Narratives are separating. The institutional review process, the one that actually controls where pension and endowment capital ends up on a ten-year horizon, has concluded what bitcoiners have been saying for a decade. Bitcoin is not crypto, and treating it as crypto has been the biggest analytical mistake in finance since the label was coined.

The Shift in the Room

The clearest signal that this sorting is being acknowledged by serious people came last Tuesday, when Admiral Samuel Paparo, Commander of US Indo-Pacific Command, sat in front of the Senate Armed Services Committee and said, in plain language, that "bitcoin is a reality." He described the protocol as a computer science breakthrough with meaningful applications, spoke about it in genuinely positive terms, and the following day confirmed that his command is running a live node on the bitcoin network. Five years ago any one of those three things, inside that room, would have been unthinkable. Last week all three happened inside forty-eight hours.

The institutional review of this technology, at the level of the state, has reached conclusions that the allocator community is still debating, and those conclusions are starting to get said out loud by people whose time on the record is scarce and reserved for things that actually matter.

Closing the Loop

At the level of the portfolio, the number of variables that can impair every traditional asset is multiplying, and the number of variables that can impair bitcoin is not, and the last eight weeks of price action are the simplest proof of that any allocator is likely to see.

At the level of the state, a globally neutral, cryptographically secured, energy-backed settlement network is being recognized for what it is, by people who think about adversarial environments for a living, and the recognition is beginning to show up in the places where recognition eventually becomes policy.

The rest of the digital asset landscape is being stripped of the narrative cover it borrowed from bitcoin for the last decade, and the separation is being priced in real time.

This is the visible surface of a monetary transition that has been underway for seventeen years and is now, finally, being acknowledged at the highest levels of capital allocation and national power.

Chart Of The Week

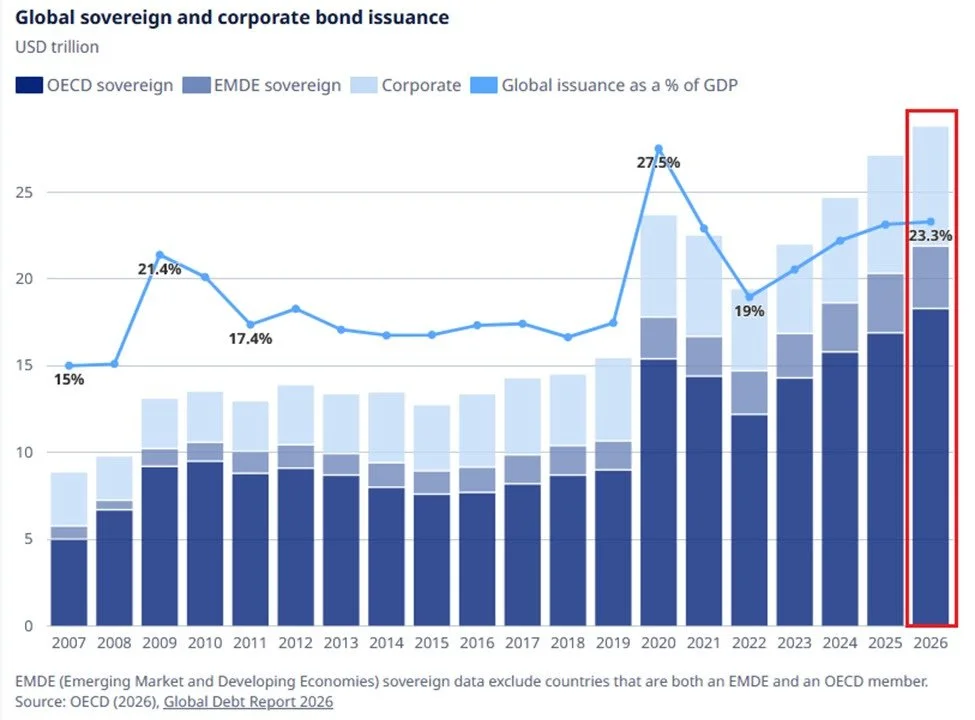

"The global debt crisis is set to get even worse: Total sovereign and corporate bond issuance is estimated to rise to a record $28.8 trillion in 2026. That would mark the 4th consecutive annual increase and would also DOUBLE the average pre-pandemic levels. Corporate debt issuance is set to surge to a record $6.9 trillion, while government debt issuance is expected to rise to $21.9 trillion, also an all-time high. By comparison, governments and corporates issued $23.7 trillion of debt in 2020, during the pandemic. As a percentage of GDP, global issuance is expected to increase to 23.3%, the 2nd-highest on record, only behind the 27.5% peak during the pandemic in 2020. To put this into perspective, the 2008 Financial Crisis peak was 21.4%. The world is borrowing ABOVE crisis levels."

Quote Of The Week

"Bitcoin is a reality. It is a peer-to-peer, zero-trust transfer of value ... Bitcoin is as a computer science tool. It's the combination of cryptography, a blockchain, and a proof of work ... We have a node on the Bitcoin network. We're doing a number of operational tests to secure and protect networks using the Bitcoin protocol."

— Admiral Paparo, Commander, US Indo-Pacific Command

Podcast Of The Week

Bitcoin For Professionals: How He Plans To Onboard 100 Million People To Bitcoin By 2030

How does a maths and physics teacher turned entrepreneur, onboard 100 million people to Bitcoin by 2030?

Subscribe to Onramp MENA’s YouTube channel to catch new episodes of the Bitcoin For Professionals podcast!

Onramp MENA is an advisory and educational platform dedicated exclusively to Bitcoin.

If Onramp MENA’s offerings align with your needs, or those of someone you know, feel free to schedule a consultation with us here.